Capital Expenditure vs Revenue Expenditure: Key Differences Explained

In more than two decades of reading balance sheets, sitting in budget meetings, and advising founders on where to put their next rupee (or dollar), I’ve noticed one thing never changes: businesses that confuse capital expenditure with revenue expenditure eventually confuse their entire financial picture. It sounds like a basic accounting distinction — the kind you’d skim past in a textbook — but get it wrong consistently, and it will quietly distort your profits, your taxes, and your valuation.

So let’s slow down and actually understand it, the way I’d explain it to a young analyst on their first week on the job.

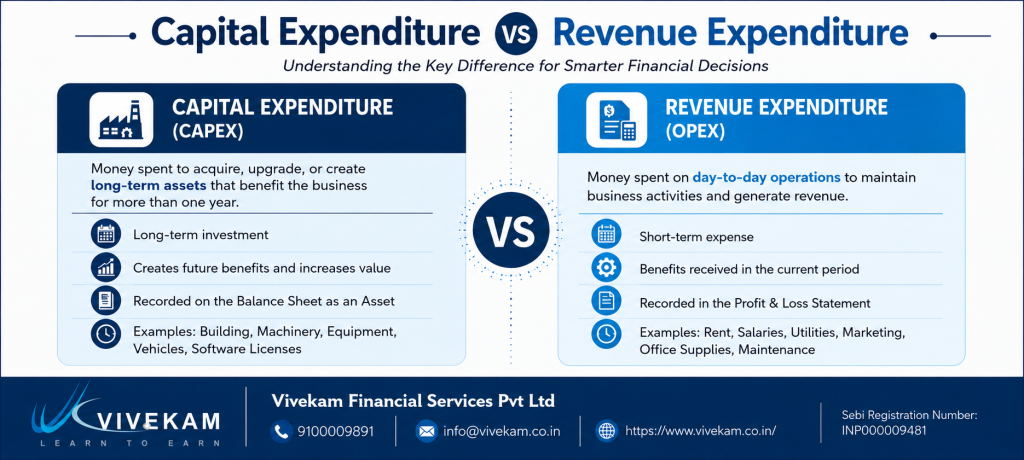

What is Capital Expenditure?

Capital expenditure, or CapEx, is money a business spends to acquire, upgrade, or extend the life of a long-term asset — something that will keep generating value for the company over several years, not just this quarter.

Think land, buildings, machinery, vehicles, or even a major software platform your company will run on for the next decade. When I evaluate a company, CapEx tells me one thing above all else: is management investing in the future, or just maintaining the present? A business that never spends on CapEx eventually stagnates. A business that overspends on it without discipline eventually runs into cash flow trouble. The art is in the balance.

Capital expenditure is capitalized on the balance sheet — meaning it isn’t expensed all at once. Instead, its cost is spread out over its useful life through depreciation or amortization. This matters because it directly affects how profitable a company appears in any given year.

What is Revenue Expenditure?

Revenue expenditure, on the other hand, is the day-to-day cost of keeping the business running. It doesn’t create a long-term asset; it simply keeps the wheels turning. Rent, salaries, utility bills, repairs, and routine maintenance all fall into this bucket.

Unlike CapEx, revenue expenditure is fully charged against the income statement in the same accounting period it’s incurred. There’s no spreading it out over years — it hits your profit and loss statement immediately.

If CapEx is about building the machine, revenue expenditure is about oiling it every single day so it keeps working.

Capital Expenditure vs Revenue Expenditure: The Core Difference

Here’s the difference between capital expenditure and revenue expenditure boiled down to what actually matters when you’re reading financial statements:

Aspect | Capital Expenditure | Revenue Expenditure |

Purpose | Acquires or improves long-term assets | Covers routine, short-term operating costs |

Benefit Period | Multiple years | Current accounting period only |

Accounting Treatment | Capitalized, then depreciated/amortized | Fully expensed immediately |

Impact on Balance Sheet | Increases asset value | No asset created |

Impact on Profit | Spread over years via depreciation | Reduces profit in the same period |

Frequency | Occasional, large-ticket | Recurring, day-to-day |

I always tell people: if you’re still using it or benefiting from it years from now, it’s probably CapEx. If it’s consumed the moment you spend it, it’s revenue expenditure.

Capital Expenditure Examples

To make this concrete, here are some classic capital expenditure examples I’ve come across across industries:

- Purchasing land or a new factory building

- Buying machinery, heavy equipment, or delivery vehicles

- Installing a new IT infrastructure or enterprise software system

- Major renovations that extend a building’s useful life

- Acquiring patents, trademarks, or long-term licenses

- Investing in research and development for a new product line

Revenue Expenditure Examples

And here are typical revenue expenditure examples that show up on almost every company’s books, month after month:

- Employee salaries and wages

- Office rent and utility bills

- Raw material purchases for production

- Routine equipment repairs and servicing

- Insurance premiums

- Marketing and advertising spend

- Interest paid on short-term loans

Types of Capital Expenditure

Not all CapEx serves the same purpose. Over the years, I’ve found it useful to bucket it into three broad types of capital expenditure:

- Expansion CapEx – spending aimed at growing the business, such as opening a new plant or entering a new market.

- Maintenance CapEx – spending required just to keep existing assets functioning at their current capacity (replacing worn-out machinery parts, for instance).

- Replacement CapEx – spending to replace old assets nearing the end of their useful life with new ones.

A seasoned investor always asks: how much of a company’s CapEx is expansion versus maintenance? A business pouring most of its capital into maintenance CapEx just to stay afloat is a very different story from one investing aggressively in expansion.

Types of Revenue Expenditure

Revenue expenditure also splits into recognizable categories:

- Direct Expenses – costs directly tied to production, like raw materials and factory wages.

- Indirect Expenses – costs that support operations but aren’t tied to a specific product, like administrative salaries, rent, and utilities.

- Maintenance Expenses – routine repair and upkeep costs that don’t extend an asset’s life, just preserve its current condition.

CapEx Formula

If you want to calculate capital expenditure straight from a company’s financial statements — something I do routinely when analyzing annual reports — use this capex formula:

CapEx = Net Increase in Property, Plant & Equipment (PP&E) + Depreciation Expense

Or, expressed differently:

CapEx = PP&E (current year) − PP&E (previous year) + Depreciation for current year

This is often pulled straight from the cash flow statement, listed under “Purchase of Property, Plant, and Equipment” in the investing activities section.

CapEx and OpEx Formula

You’ll also frequently hear CapEx discussed alongside OpEx (operating expenditure) — essentially another name for revenue expenditure in a business context. Here’s the OpEx formula for reference:

OpEx = Revenue Expenditure incurred in day-to-day operations (salaries + rent + utilities + repairs + admin costs, etc.)

And when analysts talk about total capital deployed, they often reference the combined CapEx and OpEx formula:

Total Business Spend = CapEx + OpEx

This total gives you a full picture of how much a company is spending — both to build for the future (CapEx) and to keep the lights on today (OpEx).

Why This Distinction Actually Matters

I’ve sat across the table from business owners who were convinced their company was underperforming, when in reality, they were simply misclassifying capital expenditure as revenue expenditure — dragging down reported profits unnecessarily. I’ve also seen the reverse: companies capitalizing costs that should have been expensed immediately, inflating profits and asset values in a way that eventually caught up with them during an audit.

Get this classification right, and you get:

- Accurate profitability — since revenue expenditure hits your P&L immediately, misclassifying it distorts your real margins.

- Correct tax treatment — capital expenditure and revenue expenditure are often treated very differently by tax authorities, and getting it wrong can trigger penalties or lost deductions.

- Better investment decisions — investors and lenders read your CapEx trends to judge whether you’re building for the future or simply treading water.

Frequently Asked Questions

- What is the main difference between capital expenditure and revenue expenditure? Capital expenditure creates or improves a long-term asset and is spread over years through depreciation, while revenue expenditure covers day-to-day running costs and is fully expensed in the same accounting period.

- Is CapEx good or bad for a company? Neither by default — it depends on the type. Expansion CapEx signals growth and confidence in the future, while excessive maintenance CapEx can signal aging assets that are becoming expensive to keep running. Context always matters more than the number itself.

- Can revenue expenditure become capital expenditure? Not on its own, but a routine repair can sometimes cross the line into CapEx if it substantially extends an asset’s useful life or increases its capacity, rather than just restoring it to normal working condition. This is a judgment call accountants make carefully, since it directly affects reported profit.

- How is CapEx different from OpEx? CapEx is spent on long-term assets and capitalized on the balance sheet, whereas OpEx (essentially revenue expenditure in a business context) covers recurring operational costs and is expensed immediately on the income statement.

- Where do I find a company’s CapEx in its financial statements? Look at the cash flow statement under “investing activities,” typically listed as “purchase of property, plant, and equipment.” You can also estimate it using the CapEx formula covered above.

- Why do investors care about CapEx trends? Because CapEx reveals intent. A rising CapEx trend paired with strong revenue growth usually signals a company investing in its future, while high CapEx with stagnant revenue can be a red flag worth digging into.

Conclusion

After twenty-plus years around balance sheets, my advice is simple: don’t just memorize the definitions of capital expenditure and revenue expenditure — understand the intent behind each expense. Ask yourself, “Will this benefit the business for years, or is it gone the moment it’s spent?” That one question, asked consistently, will keep your books honest, your taxes accurate, and your financial decisions sharp. Whether you’re a business owner allocating your next budget or an investor sizing up a company’s annual report, mastering this distinction is one of the simplest ways to read a business more clearly than most people ever will.