Fixed Deposit vs Recurring Deposit: What's the Difference?

I’ve been asked some version of this question more times than I can count over the last twenty-odd years — usually by someone who just got their first bonus, or a parent who wants their kid to stop keeping cash “under the mattress” and start doing something sensible with it. Fixed Deposit or Recurring Deposit?

Here’s the honest answer: it’s not really a competition. They’re two different tools for two different jobs, and confusing them is like asking whether a hammer is “better” than a screwdriver. It depends entirely on what you’re building.

So let’s slow down and actually understand Fixed Deposit vs Recurring Deposit — not as a checklist, but as two instruments I’d happily recommend to my own family, depending on their situation. We’ll cover the benefits, the disadvantages nobody likes to mention, the real interest-rate math, and finally, a straight answer to RD or FD which is better — no fence-sitting.

What is a Fixed Deposit Account?

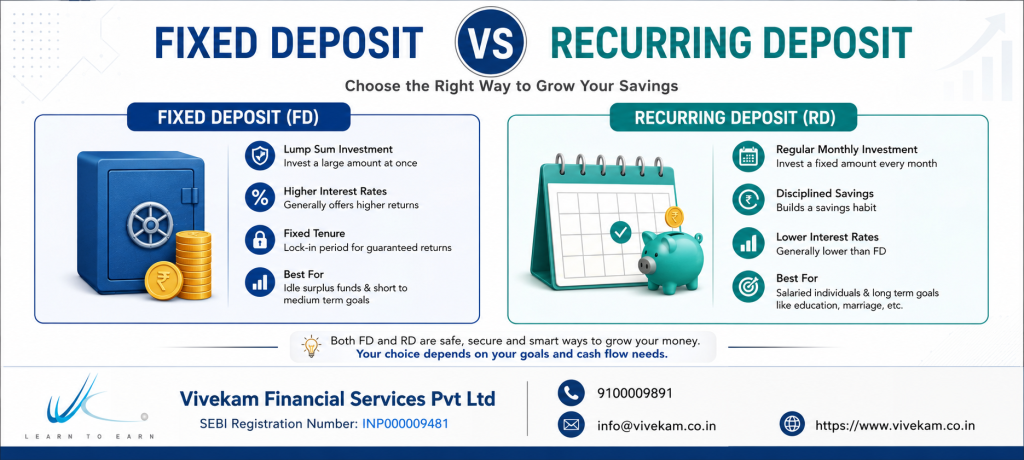

A Fixed Deposit is the simplest promise a bank can make you: hand over a lump sum today, agree not to touch it for a set period, and the bank pays you a fixed rate of interest for the privilege. The FD full form — Fixed Deposit — tells you exactly what you’re getting. Fixed amount in, fixed rate, fixed tenure. No surprises, which, after enough years in this business, I’ve learned to appreciate more than most people realize.

The catch — and there’s always a catch — is that once the money is in, it’s in. You can’t top it up like a savings account. It just sits there, quietly compounding, until maturity or until you break it early (and pay for that decision). I’ve always thought of an FD less as an “investment” and more as a vault with a timer on it. It’s not going to make you rich. It’s going to make sure you don’t lose what you already have.

Types of Fixed Deposit

Not every FD is cut from the same cloth. Over the years I’ve used almost every variant on this list, and each one earns its place for a specific reason:

- Standard/Regular FD – Your bread-and-butter option. Pick a tenure anywhere from 7 days to 10 years and let it run.

- Tax-Saving FD – Locks your money for 5 years, no exceptions, but earns you a deduction under Section 80C. Good discipline if you tend to spend what you can touch.

- Senior Citizen FD – Banks pay retirees 0.25%–0.75% more, and rightly so — this is often the safest income stream in a retiree’s portfolio.

- Cumulative FD – Interest compounds and pays out in one lump sum at the end. My preference when I don’t need the income right now.

- Non-Cumulative FD – Pays interest monthly, quarterly, or annually. This is what I’d point a retiree toward if they need a regular paycheck substitute.

- Flexi FD – Tied to your savings account, so you can pull out a portion without cracking open the whole deposit. Useful, underused.

- NRI Fixed Deposit – NRE, NRO, or FCNR accounts built specifically for money earned or held abroad.

What is a Recurring Deposit Account?

If an FD is a vault, a Recurring Deposit is a habit with interest attached. The RD full form is Recurring Deposit, and it works exactly the way it sounds — you commit to depositing a fixed sum every month for a set tenure, and the bank pays you interest on the growing balance, usually compounded quarterly.

I’ve told younger investors for years: most people don’t fail to build wealth because they picked the wrong instrument — they fail because they never developed the discipline to save consistently. An RD forces that discipline on you. You don’t need a windfall to start one; you need ₹500 and the willpower to repeat it every month without fail.

By the time the tenure ends, you’re holding a lump sum you’d probably never have accumulated by “saving whatever’s left over” — which, in my experience, is usually nothing.

Difference between FD and RD

Enough theory. Let’s put them side by side, the way I’d sketch it on a napkin for a client:

Parameter | Fixed Deposit (FD) | Recurring Deposit (RD) |

Investment Type | Lump sum, one-time deposit | Fixed monthly installments |

Ideal For | Investors with a lump sum amount | Investors who want to save monthly |

Tenure | 7 days to 10 years | 6 months to 10 years |

Interest Rate | Slightly higher in most banks | Comparable, sometimes marginally lower |

Liquidity | Premature withdrawal allowed with penalty | Premature withdrawal allowed with penalty |

Minimum Investment | Varies by bank (often ₹1,000–₹10,000) | Usually starts as low as ₹100–₹500/month |

Interest Payout | Monthly, quarterly, annually, or at maturity | Usually paid at maturity along with principal |

Tax Benefit | Available only in Tax-Saving FD (5-year lock-in) | No specific tax-saving RD option |

Risk | Low (guaranteed returns) | Low (guaranteed returns) |

Look at that table long enough and the decision starts making itself. The real question isn’t which one is “better” in the abstract — it’s whether you’re sitting on a lump sum or building one. That single fact, more than any interest rate, tells you which side of fixed deposit vs recurring deposit you belong on.

FD Interest Rate vs RD Interest Rate

Everyone wants to know the number before they’ve even decided what they’re investing for — I get it, so let’s talk numbers.

In most banks, the FD interest rate sits marginally above the RD interest rate, and there’s a simple reason for it, not some marketing trick: with an FD, the bank has your full principal from day one. With an RD, it only ever holds an average of roughly half your eventual total at any given time, since your money trickles in monthly. The bank’s cost of funds is different, so the rate reflects that.

Rough ranges you’ll see quoted across banks today:

- FD interest rate: roughly 6% to 7.75% per annum, depending on the bank, tenure, and depositor category.

- RD interest rate: roughly 6% to 7.5% per annum — close enough to FD rates that the gap rarely decides anything on its own.

Here’s the part most articles skip: on a ₹1,00,000 FD at 7% for 5 years, compounded quarterly, you’d walk away with roughly ₹1,41,000 — about ₹41,000 in interest, untouched by your effort after day one. An RD of ₹1,667 a month for the same 5 years at a similar rate builds you to a similar ballpark, but you’ve earned less interest on your total contribution simply because your money spent less time compounding, on average, than a lump sum would.

That’s not a flaw in the RD — it’s just physics. Money that sits longer earns more. Senior citizens get an extra 0.25%–0.75% on either instrument, which I’d always tell a retiree to ask about explicitly, because banks don’t always volunteer it. And since rates move with RBI policy, treat any number you read — including mine — as a starting point, not gospel. Confirm the current rate with your bank before you sign anything.

Fixed Deposit Benefits

If you strip away the marketing language, the Fixed Deposit benefits that actually matter to a long-term investor come down to a short list:

Certainty. The rate you’re quoted on day one is the rate you get, market crashes and all. I’ve watched people panic-sell equities during downturns and wish, in that exact moment, that some portion of their money had been sitting somewhere boring. That’s what an FD is for.

Flexibility of tenure. Anywhere from 7 days to 10 years means you can park emergency cash for a month or lock away retirement savings for a decade — same instrument, different horizon.

A genuine edge for senior citizens — that 0.25%–0.75% bump sounds small until you realize it compounds over a decade of retirement income.

A loan sitting quietly in reserve. Most people don’t realize you can borrow against your own FD instead of breaking it. I’ve used this more than once to bridge a short cash-flow gap without sacrificing years of compounding.

A legitimate tax lever, in the form of the 5-year tax-saving FD under Section 80C — not the most exciting deduction available, but a reliable one.

Insurance you don’t have to think about. Deposits up to ₹5 lakh are covered under DICGC, which is more protection than most people realize they already have.

The choice between cumulative and non-cumulative payouts — compound it all for later, or draw it as income now. Few instruments let you decide that upfront.

Recurring Deposit Benefits

I’ll be blunt about the biggest Recurring deposit benefits: the money matters less than the behavior it builds.

It manufactures discipline. You don’t need willpower to save if the bank simply debits the amount every month. That’s the whole trick, and it works better than any budgeting app I’ve seen.

The entry point is almost embarrassingly low. Some banks will let you start with a few hundred rupees a month. There’s no excuse of “I don’t have enough to invest” left standing after that.

The rate is locked in, same as an FD — no surprises halfway through your tenure.

Tenures run from 6 months to 10 years, so an RD can just as easily fund next year’s vacation as it can a child’s future school fees.

You can borrow against it, same courtesy extended to FD holders, without losing your accumulated interest.

It’s genuinely goal-shaped. I’ve recommended RDs specifically for things with a known date and a known cost — a wedding, a down payment, a planned purchase.

And it carries the same DICGC insurance up to ₹5 lakh as an FD — safety isn’t sacrificed for convenience here.

FD Disadvantages

Now, the part most brochures conveniently leave out. Here are the real FD disadvantages, the ones I’d want someone to tell me before I signed the form:

You need the lump sum first. No lump sum, no FD — simple as that, and it rules out a lot of people who are trying to build savings from scratch.

Breaking it early costs you. Life happens, and if you need that money before maturity, expect a penalty and a lower effective rate. I’ve seen people lose more to premature withdrawal than they ever gained in interest.

It will not make you wealthy. Compare FD returns to a couple of decades of equity market returns and the gap is not subtle. An FD protects capital; it does not grow it aggressively. Don’t confuse the two jobs.

The taxman doesn’t care that your return was “fixed.” Interest is taxed at your slab rate, and TDS kicks in once you cross the threshold — so that quoted rate is never quite what lands in your account.

Inflation doesn’t pause for your FD. A 7% return sounds fine until inflation runs at 6%, and you realize your real, inflation-adjusted gain was barely worth the five-year wait.

And once it’s opened, it’s closed to new money. Want to add more? You’re opening a fresh FD, not topping up the old one.

RD Disadvantages

The discipline that makes an RD attractive is the same thing that trips people up. The honest RD disadvantages:

The discipline cuts both ways. Miss a monthly installment and you’re usually looking at a penalty. The instrument that builds good habits punishes you the moment the habit slips.

Your money compounds for less time, on average, than a lump sum would. Since deposits trickle in monthly rather than all at once, the total interest earned trails a comparable FD — not because the rate is worse, but because less money was actually invested for most of the tenure.

Tax doesn’t skip RDs either. Interest is taxable and TDS applies just as it does with an FD — nobody gets a free pass here.

Closing it early costs you, same story as an FD: a lower rate and, often, a penalty on top.

There’s no tax-saving version of this instrument. If Section 80C deductions matter to you, the RD simply doesn’t play in that game — you’ll need the tax-saving FD for that.

And you’re locked into a monthly commitment for the full tenure, which can pinch during a tight month if you haven’t budgeted for it properly.

RD or FD Which is Better?

Let me give you the verdict I’d actually give a client sitting across the table, not a diplomatic “it depends.”

If you already have the money sitting idle — a bonus, an inheritance, proceeds from selling something — put it in an FD. There is no reason to let a lump sum sit in a savings account earning next to nothing while you “decide what to do with it.” Decide today: FD it, and go on with your life.

If you don’t have the lump sum yet, but you have a salary, an RD is not the consolation prize — it’s the correct tool. I’d go further: an RD is often the single most underrated instrument for anyone under 35 who hasn’t yet built the habit of saving before spending.

And if you’re asking me what I’d actually do — I wouldn’t choose one. I’d run both, permanently, side by side. Every windfall goes into a fresh FD. Every salary cycle feeds an RD. Over enough years, the FDs become your safety net and the RDs become the pipeline that keeps refilling it. That’s not indecision — that’s just how disciplined money actually behaves.

Conclusion

After twenty-plus years of watching people make this decision, here’s what I know for certain: nobody ever regretted having some boring, guaranteed money sitting quietly in the background while the rest of their portfolio took bigger swings. Fixed Deposits and Recurring Deposits aren’t exciting. They were never meant to be. Their job is to be the one part of your financial life that behaves exactly as promised, every single time.

The difference between FD and RD really comes down to one honest question: do you have the money already, or are you building toward it? An FD rewards what you’ve already accumulated. An RD builds the discipline to accumulate more. Both deserve a place in a serious financial plan.

Chase the best FD interest rate you can find for money you already have. Commit to the best RD interest rate for money you’re about to earn. And stop treating RD or FD which is better as a debate — treat it as a division of labor. That’s how the money actually grows.

FAQs

- What is the FD full form and RD full form?

FD full form — Fixed Deposit. RD full form — Recurring Deposit. Simple names, and refreshingly, they don’t lie to you about what’s inside. - What is the main difference between FD and RD?

One check versus twelve. That’s the entire difference between FD and RD in practice — an FD is a single lump sum locked away, an RD is a monthly commitment building toward one. - Which offers a higher interest rate, FD or RD?

The FD interest rate typically edges out the RD interest rate, and it’s simple economics — the bank has your full money from day one with an FD, whereas an RD only builds up gradually. - Can I withdraw my FD or RD before maturity?

You can, but I’d think twice. Both come with a penalty and a reduced rate for breaking early — the bank is essentially charging you for changing your mind. - Is the interest earned on FD and RD taxable?

Every rupee of it, at your income slab rate, with TDS deducted once you cross the threshold. Don’t let the word “fixed” fool you into thinking the taxman forgot about it. - Which is better for beginners — FD or RD?

If you’re starting from zero, an RD teaches you the one skill that actually matters long-term: consistency. Save the FD conversation for the day you have a lump sum to protect. - Can senior citizens get higher interest rates on FD and RD?

Yes — typically 0.25% to 0.75% more on both. I’ve never met a retiree who shouldn’t be asking their bank about this explicitly. - Is there a tax-saving RD option like a tax-saving FD?

No. If Section 80C deductions are part of your plan, that road runs through the 5-year tax-saving FD, not the RD. - What is the minimum tenure for FD and RD?

FDs can start as short as 7 days. RDs generally start at 6 months. Neither demands a decade-long commitment if you don’t want one. - Can I take a loan against my FD or RD?

Yes, on both. It’s one of the more underused tricks in personal finance — a way to access cash without ever breaking your compounding.

Disclaimer: Interest rates for FD and RD vary across banks and change periodically based on RBI policies. Please check with your respective bank or financial institution for the latest rates before investing.