Equity Share vs Preference Share: Meaning, Types, and Differences

If you’ve ever wondered how companies like Reliance Industries, Infosys, or Tata Motors raise thousands of crores without taking massive bank loans, the answer often lies in one word—shares.

When a company needs money to expand its business, build new factories, acquire another company, or invest in research and development, it has multiple financing options. It can borrow money through loans or issue shares to investors. Among the various types of shares available, equity shares and preference shares are the two most important.

At first glance, both may look similar because they represent ownership in a company. However, they serve completely different purposes. Equity shareholders become the true owners of the business and participate in its growth, while preference shareholders enjoy priority in dividend payments but usually sacrifice voting rights and unlimited upside.

This distinction isn’t just theoretical. It influences how companies structure their finances and how investors choose where to put their money. An aggressive investor looking for long-term wealth creation will usually lean toward equity shares, whereas someone seeking predictable income may find preference shares more suitable.

In this guide, we’ll go beyond textbook definitions. You’ll learn what is equity share, what is preference share, their features, different types, advantages, and the complete difference between equity share and preference share—explained the way experienced finance professionals actually think about them.

Introduction to Company Shares

Imagine you’re launching a manufacturing business that requires ₹500 crore to build a new production facility. Borrowing the entire amount from a bank would mean paying interest regardless of whether your business earns profits. That can become a heavy financial burden.

Instead, you may invite investors to contribute capital in exchange for ownership. Those investors become shareholders.

From a company’s perspective, issuing shares reduces dependence on debt and strengthens its financial position. From an investor’s perspective, buying shares is an opportunity to participate in the company’s future success.

Broadly, companies raise equity capital through two primary categories of shares:

- Equity Shares

- Preference Shares

Although both help businesses raise long-term capital, they differ significantly in terms of ownership rights, dividends, voting power, and risk. Understanding these differences is essential for anyone studying finance, preparing for professional exams, or investing in the stock market.

What is Equity Share?

Meaning of Equity Shares

The simplest way to understand equity shares is to think of them as ownership certificates.

When you purchase an equity share, you aren’t lending money to the company—you are buying a small piece of the business itself. Whether you own ten shares or ten lakh shares, you become one of its owners.

That’s why equity shareholders are often referred to as residual owners. After the company pays salaries, suppliers, taxes, lenders, and preference shareholders, whatever profits remain ultimately belong to equity shareholders.

This also explains why investing in equity is both exciting and risky.

If the company grows consistently over the next decade, launches successful products, expands globally, and increases its profits, equity shareholders benefit through rising share prices, increasing dividends, bonus shares, and wealth creation.

However, if the company struggles, profits decline, or the business fails, equity shareholders bear the greatest risk because they are the last to receive any remaining assets during liquidation.

This balance between risk and reward is what makes equity investing one of the most powerful long-term wealth-building tools available.

Features of Equity Shares

Understanding the features of equity shares helps explain why they remain the most popular investment instrument across global stock markets.

1. Ownership in the Company

Unlike bondholders or lenders, equity shareholders own a part of the business. Every share represents a fractional ownership interest.

For example, if a company has one crore outstanding shares and you own one lakh shares, you own approximately 1% of the company.

2. Voting Rights

One of the biggest advantages of holding equity is the right to vote on important corporate decisions.

Shareholders may vote on matters such as:

- Appointment of directors

- Mergers and acquisitions

- Major restructuring decisions

- Changes in company policies

- Approval of certain corporate actions

While retail investors usually own too few shares to influence decisions individually, institutional investors and promoters actively exercise these rights.

3. No Fixed Dividend

Many beginners mistakenly believe companies must pay dividends every year.

That’s not true.

Unlike interest on a loan, dividends are entirely discretionary. The board of directors decides whether profits should be distributed among shareholders or retained to finance future growth.

Fast-growing companies often prefer reinvesting profits rather than paying large dividends. That’s one reason many successful technology companies historically focused more on capital appreciation than dividend payouts.

4. Unlimited Wealth Creation Potential

This is where equity investing becomes truly attractive.

Suppose you invested in a fundamentally strong company twenty years ago when its shares traded at ₹100. If the business consistently increased its profits, expanded operations, and created shareholder value, that investment could be worth several thousand rupees per share today.

Unlike fixed-income investments, equity returns have no upper limit because they’re directly linked to business growth.

5. Higher Investment Risk

Higher returns always come with higher uncertainty.

The market value of equity shares changes every trading day based on factors such as:

- Company earnings

- Industry performance

- Economic conditions

- Interest rates

- Investor sentiment

- Global events

This volatility can make equity investing emotionally challenging for beginners. However, experienced investors understand that short-term price movements are often less important than long-term business performance.

6. Residual Claim During Liquidation

This feature explains why equity shareholders are rewarded with potentially higher returns.

If a company is liquidated, payments are made in a specific order:

- Secured creditors

- Banks and financial institutions

- Bondholders

- Employees and statutory dues

- Preference shareholders

- Equity shareholders

Whatever remains—if anything—is distributed among equity shareholders.

Because they stand last in line, they assume the highest risk and therefore expect the highest long-term returns.

Types of Equity Shares

There isn’t just one category of equity ownership. Depending on the company’s objectives, different types of equity shares may be issued.

1. Ordinary Equity Shares

These are the standard shares traded on stock exchanges. They carry voting rights and entitle shareholders to dividends whenever declared by the company.

Most retail investors own ordinary equity shares.

2. Rights Shares

Sometimes companies need additional capital but want to reward existing shareholders before approaching new investors.

In such cases, they issue rights shares, allowing current shareholders to purchase additional shares—often at a discount to the prevailing market price.

Rights issues help companies raise capital while giving loyal shareholders the opportunity to maintain their ownership percentage.

3. Bonus Shares

A bonus issue doesn’t require shareholders to invest additional money.

Instead, the company converts a portion of its accumulated reserves into share capital and distributes extra shares free of cost.

For example, in a 1:1 bonus issue, every shareholder receives one additional share for every existing share held.

Although the number of shares increases, the overall value of the investment generally remains unchanged immediately after the bonus issue because the share price adjusts accordingly.

4. Sweat Equity Shares

Companies often reward employees or key executives who create exceptional value for the business.

Instead of paying them entirely in cash, they may issue sweat equity shares in recognition of their technical expertise, innovation, or intellectual property contributions.

This aligns employee interests with long-term shareholder value.

5. Shares with Differential Voting Rights (DVR Shares)

Not every equity share carries identical voting power.

Some companies issue Differential Voting Rights (DVR) shares that provide either reduced voting rights with higher dividends or vice versa.

These instruments help companies raise capital while allowing promoters to retain greater control over management decisions.

Advantages of Equity Shares

The popularity of equity investing isn’t accidental. Over long periods, equity has consistently outperformed most traditional investment options because it allows investors to participate directly in business growth.

Some of the major advantages of equity shares include:

Opportunity for Long-Term Wealth Creation

History has repeatedly shown that businesses creating sustainable profits also create substantial shareholder wealth. Investors who remain patient often benefit from compounding over decades rather than years.

Capital Appreciation

Unlike fixed-income investments that generate predetermined returns, equity shares can appreciate significantly as the company’s earnings and market valuation increase.

Ownership and Voting Rights

Equity investors aren’t merely financiers—they are owners with a voice in major corporate decisions.

Liquidity

Listed equity shares can generally be bought and sold easily through stock exchanges, giving investors flexibility to enter or exit their investments.

Bonus and Rights Benefits

Companies may reward shareholders through bonus issues or provide opportunities to purchase additional shares through rights issues.

Inflation-Beating Returns

One of equity’s greatest strengths is its ability to outpace inflation over long investment horizons. As companies grow their revenues and profits, shareholders often benefit from increasing business value, helping preserve and grow purchasing power.

What is Preference Share?

Meaning of Preference Shares

If equity shareholders are the entrepreneurs of a company, preference shareholders are closer to conservative investors who value stability over spectacular returns.

To understand what is preference share, imagine lending money to a company—but with a twist. You’re not a lender, because you’re still investing through shares. At the same time, you’re not a full-fledged owner like an equity shareholder either.

Preference shares sit comfortably between debt and equity, which is why finance professionals often describe them as a hybrid security.

The biggest attraction of preference shares is exactly what the name suggests—they enjoy preference.

That preference comes in two important ways:

- They receive dividends before equity shareholders.

- If the company is liquidated, they get their capital back before equity shareholders.

However, every financial advantage comes with a trade-off.

Unlike equity investors, preference shareholders usually don’t enjoy voting rights. More importantly, if the company suddenly becomes the next Infosys or Reliance Industries, preference shareholders generally don’t participate in that explosive wealth creation because their returns are largely fixed.

This is why companies often issue preference shares when they want to raise long-term capital without diluting management control. Since preference shareholders usually cannot influence major business decisions, promoters retain greater control over the company.

For investors, preference shares are often suitable when the priority is steady income rather than aggressive capital appreciation.

Features of Preference Shares

Understanding the features of preference shares makes it easier to see why they appeal to a completely different class of investors than equity shares.

1. Priority in Dividend Payments

This is the defining characteristic.

Suppose a company earns a profit of ₹100 crore.

Before the board even considers paying dividends to equity shareholders, it must first pay the agreed dividend to preference shareholders.

If no dividend is declared for equity shareholders, preference shareholders may still receive theirs depending on the terms of issue.

This makes preference shares relatively more predictable.

2. Fixed Dividend Rate

Unlike equity dividends, which fluctuate based on profitability and management decisions, preference shares usually carry a predetermined dividend rate.

For example, if a company issues 8% preference shares, investors know in advance what dividend they are entitled to receive, provided the company declares dividends according to the applicable terms.

This predictability attracts investors who prefer stable cash flows.

- Priority During Liquidation

One of the first lessons I teach young investors is this:

Always ask who gets paid first if things go wrong.

In corporate finance, that order matters.

If a company is wound up, creditors are paid first, followed by preference shareholders, and only then do equity shareholders receive whatever remains.

This additional layer of protection is one reason preference shares are considered less risky than equity shares.

4. Limited Voting Rights

Preference shareholders generally don’t participate in day-to-day corporate governance.

They usually cannot vote on:

- Appointment of directors

- Business strategy

- Mergers

- Corporate restructuring

However, company law in many jurisdictions grants them voting rights in specific situations—for example, when matters directly affect their rights or when dividends remain unpaid for a prescribed period.

5. Lower Risk, Lower Reward

There’s no such thing as a free lunch in investing.

The reduced risk associated with preference shares comes at the cost of limited upside.

Even if the company’s profits double over the next five years, preference shareholders generally continue receiving only their fixed dividend.

Equity shareholders, on the other hand, enjoy the benefit of rising earnings and increasing market valuations.

6. Hybrid Nature

Preference shares combine characteristics of both debt and equity.

Like debt:

- They usually provide fixed returns.

Like equity:

- They form part of shareholders’ funds.

- They don’t require mandatory repayment like bank loans unless they’re redeemable.

This hybrid structure gives companies greater flexibility in managing their capital.

Types of Preference Shares

Not all preference shares are identical. Companies design them differently depending on financing needs and investor expectations.

Let’s explore the most common types of preference shares.

1. Cumulative Preference Shares

Imagine a company faces a difficult financial year and cannot pay dividends.

With cumulative preference shares, those unpaid dividends don’t disappear.

Instead, they accumulate and must be paid before any dividend is distributed to equity shareholders in future profitable years.

This additional protection makes cumulative preference shares particularly attractive to conservative investors.

2. Non-Cumulative Preference Shares

Here, unpaid dividends do not carry forward.

If the company skips dividends in a particular year, investors lose that year’s dividend permanently.

Future dividends are unaffected, but past unpaid amounts cannot be claimed.

3. Participating Preference Shares

These shares offer something extra.

After receiving their fixed dividend, participating preference shareholders may also receive an additional share of profits if the company performs exceptionally well.

Although less common, they provide a balance between fixed income and growth participation.

4. Non-Participating Preference Shares

These shareholders receive only the fixed dividend mentioned in the share terms.

Even if the company earns record profits, they don’t receive any additional distribution.

Most preference shares issued by companies fall into this category.

5. Convertible Preference Shares

These shares provide flexibility.

After a specified period—or upon meeting certain conditions—they can be converted into equity shares.

This allows investors to begin with relatively stable returns while retaining the option to participate in future business growth.

Many startups and private equity transactions use convertible instruments because they balance investor protection with long-term upside.

6. Non-Convertible Preference Shares

As the name suggests, these cannot be converted into equity shares.

They remain preference shares throughout their tenure.

7. Redeemable Preference Shares

Most preference shares issued today are redeemable.

The company repurchases them after a predetermined period according to the issue terms.

From a corporate finance perspective, redeemable preference shares allow businesses to raise capital without creating permanent ownership dilution.

8. Irredeemable Preference Shares

Historically, some companies issued irredeemable preference shares that remained outstanding indefinitely.

However, under modern company laws in countries like India, issuing irredeemable preference shares is generally not permitted.

Advantages of Preference Shares

The advantages of preference shares make them suitable for investors who value certainty over aggressive wealth creation.

Predictable Dividend Income

One of the biggest attractions is the possibility of receiving fixed dividends, making financial planning easier.

Lower Volatility

Preference shares generally experience smaller price fluctuations than equity shares because investor expectations are centred more on income than rapid growth.

Priority Over Equity Shareholders

Whether it’s dividend distribution or liquidation proceeds, preference shareholders enjoy preferential treatment.

That additional safety margin is valuable during periods of economic uncertainty.

Suitable for Conservative Investors

Retirees, income-focused investors, and institutions seeking relatively stable returns often consider preference shares as part of their diversified portfolio.

Potential Conversion Benefits

Convertible preference shares offer investors the best of both worlds—initial stability with the possibility of future equity participation.

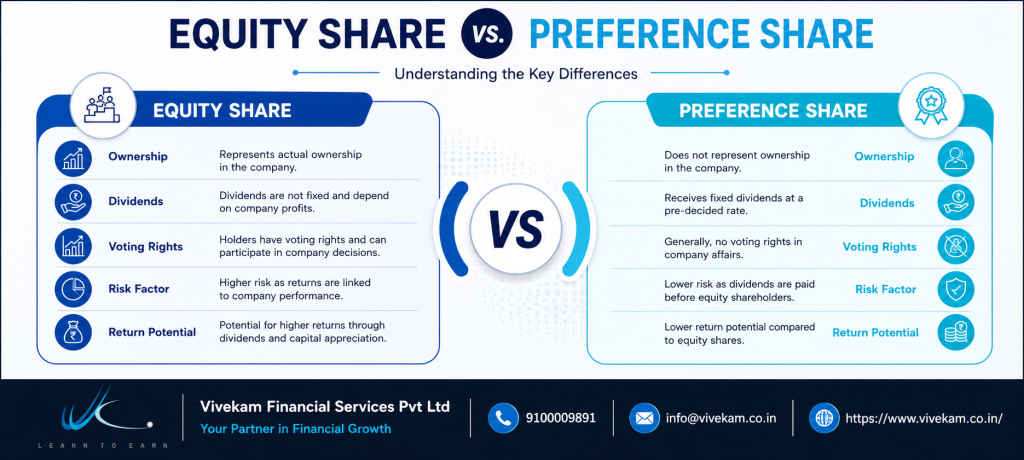

Equity Share vs Preference Share

Now that we’ve explored both instruments individually, let’s compare them from an investor’s perspective.

The difference between equity share and preference share isn’t simply about dividends or voting rights. It reflects two completely different investment philosophies.

One focuses on wealth creation.

The other focuses on income stability.

Difference Between Equity Share and Preference Share

|

Basis |

Equity Shares |

Preference Shares |

|

Ownership |

Represents true ownership in the company. |

Represents preferential ownership with limited rights. |

|

Dividend |

Variable and depends on profits. |

Usually fixed and paid before equity dividends. |

|

Voting Rights |

Full voting rights on important corporate matters. |

Generally no voting rights except in special situations. |

|

Risk |

Higher because shareholders are last in the repayment hierarchy. |

Comparatively lower due to preferential treatment. |

|

Return Potential |

Unlimited if the business grows significantly. |

Limited because returns are generally fixed. |

|

Capital Appreciation |

High long-term appreciation potential. |

Limited appreciation in most cases. |

|

Liquidation |

Paid only after all creditors and preference shareholders. |

Paid before equity shareholders. |

|

Business Control |

Can influence corporate decisions through voting. |

Usually no management control. |

|

Ideal Investor |

Long-term wealth builders willing to accept market volatility. |

Investors seeking stable income with relatively lower risk. |

|

Market Behaviour |

Prices fluctuate significantly based on business performance and investor sentiment. |

Prices are comparatively stable because returns are largely fixed. |

Similarities Between Equity and Preference Shares

Despite their differences, both instruments share several common characteristics.

- Both represent a company’s share capital.

- Both help businesses raise long-term funds.

- Both are issued under the Companies Act and SEBI regulations (for listed companies in India).

- Both may provide dividend income, although under different conditions.

- Both can form part of an investor’s diversified portfolio depending on financial goals.

The key difference lies not in ownership itself but in the rights attached to that ownership.

Examples of Equity and Preference Shares

Let’s bring the concept into the real world.

Imagine ABC Manufacturing Ltd. plans to build a new production facility requiring ₹1,000 crore.

Instead of borrowing the entire amount, the company decides to raise:

- ₹700 crore through equity shares

- ₹300 crore through preference shares

The equity investors accept greater uncertainty because they believe the expansion will substantially increase profits over the next decade.

The preference investors, however, are less interested in extraordinary growth. Their priority is receiving a fixed dividend with relatively greater protection.

Now suppose the expansion becomes hugely successful.

The company’s profits triple.

The share price doubles over five years.

Who benefits the most?

The equity shareholders.

Their investment grows through both capital appreciation and potentially higher dividends.

Preference shareholders continue receiving their agreed dividend but usually don’t participate fully in the company’s dramatic increase in value.

This simple example captures the core distinction between growth investing and income investing.

Which Share Should Investors Choose?

There’s no universal answer.

The better question is:

What are you trying to achieve with your investment?

Choose equity shares if you:

- Want long-term wealth creation.

- Can tolerate market volatility.

- Have an investment horizon of at least five to ten years.

- Believe in the growth potential of fundamentally strong businesses.

Choose preference shares if you:

- Prefer relatively predictable income.

- Want lower investment risk.

- Value stability more than aggressive returns.

- Need regular cash flows for financial planning.

In practice, experienced investors rarely think in absolutes.

A well-diversified portfolio often combines growth-oriented equity investments with income-generating assets depending on age, financial goals, and risk appetite.

Common Mistakes to Avoid While Investing

Over the years, I’ve noticed the same mistakes repeated by new investors.

- Assuming fixed dividends mean guaranteed returns.

- Ignoring the financial health of the issuing company.

- Investing based solely on dividend percentage.

- Chasing short-term stock price movements instead of business fundamentals.

- Confusing preference shares with bonds.

- Ignoring taxation and liquidity before investing.

The quality of the company matters far more than the label attached to the security.

Frequently Asked Questions (FAQs)

1. What is equity share?

An equity share represents ownership in a company. Equity shareholders have voting rights and participate in the company’s profits through dividends and capital appreciation.

2. What is preference share?

A preference share is a class of share that gives investors priority in dividend payments and capital repayment over equity shareholders, usually in exchange for limited voting rights.

3. What are the types of equity shares?

The major types of equity shares include ordinary shares, rights shares, bonus shares, sweat equity shares, and shares with differential voting rights (DVR).

4. What are the types of preference shares?

The common types of preference shares are cumulative, non-cumulative, participating, non-participating, convertible, non-convertible, redeemable, and irredeemable preference shares.

5. Which is better: equity share vs preference share?

Neither is universally better. Equity shares suit investors seeking long-term growth, while preference shares are generally better for those prioritizing relatively stable income and lower risk.

6. Why do companies issue preference shares?

Companies issue preference shares to raise long-term capital without significantly diluting voting control. They can also strengthen their capital structure without increasing debt obligations.

Conclusion

Understanding equity share vs preference share isn’t just about passing an exam or learning financial terminology. It’s about understanding how businesses raise capital and how investors participate in that journey.

If your objective is long-term wealth creation and you’re comfortable with market fluctuations, equity shares have historically been the stronger vehicle because they allow you to participate directly in a company’s growth. Every successful business—from consumer brands to technology giants—has rewarded patient equity investors over time.

On the other hand, preference shares serve a different purpose. They appeal to investors who value stability, predictable income, and priority over equity shareholders in dividends and liquidation. While they may not generate extraordinary returns, they can play an important role in a balanced investment strategy.

The most successful investors don’t ask which instrument is universally better. They ask which one aligns with their financial goals, risk tolerance, and investment horizon. Once you understand that distinction, choosing between equity shares and preference shares becomes much simpler—and much smarter.